Q2 affordability obstacles hinder would-be first-time home buyers

By Elizabeth Renter | NerdWallet

Home prices may have come down from their 2022 high, but they remained out of reach for the typical would-be first-time buyer in the second quarter, especially in the nation’s most populous areas.

Buying a home in this market can be particularly hard for people who haven’t done it before. First-time buyers traditionally have lower incomes and less established credit than repeat home buyers. Further, they generally make smaller down payments — 8%, on average, according to the most recent Profile of Buyers & Sellers from the National Association of Realtors, compared with 19% for repeat buyers. Buying a first home has arguably never been easy, but it’s gotten extremely difficult under current conditions.

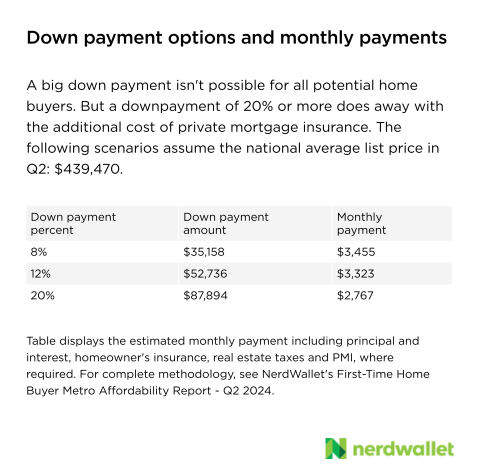

With a down payment of 8%, housing payments on a typically priced home in the second quarter of 2024 would equate to almost half of the median gross monthly income for Americans of first-time buyer age.

Making a larger down payment or choosing a less desirable home could make this initial purchase easier, but not all homebuying hopefuls will find those options possible.

Housing payments for first-time buyers: 49% of income

The average sticker price for a home in the second quarter of this year was $439,000, according to NerdWallet analysis of Realtor.com data. But the advertised price of a home is far from the only consideration of affordability.

For that reason, we examined the potential housing payment for first-time buyers in the second quarter. This payment not only accounts for the price of the home, but also the typical first-time buyer down payment, mortgage rate, real estate taxes, homeowners insurance and PMI, or private mortgage insurance — a requirement on conventional mortgages financed with less than 20% down.

That estimated monthly housing payment using the nationwide average home price was close to $3,500 in the second quarter of the year. That’s 49% of the median income for Americans in the first-time home buyer age group. And estimated payments in some of the country’s largest metro areas were considerably higher.

First-time home buyer tip: In the highest-priced markets such as Los Angeles, New York and San Diego, putting 8% down on a home may not be feasible. That’s because typical home prices in these areas are well over one million dollars, and would require what’s known as a jumbo mortgage. Currently, loans over $766,550 exceed the cap for conforming loans, according to the Federal Housing Finance Agency, and jumbo loans generally have stricter standards, including larger down payment requirements. Buyers in these markets will need higher-than-average incomes, larger down payments and flexibility on their side to become homeowners.

In other areas, buyers hoping to put less than 20% of the sale price down have more options. Many lenders offer loans with lower down payments — as low as 3% — and most states have first-time home buyer programs with benefits such as down payment assistance.

Buyers (and borrowers) have a few options

One lesson that became apparent to home buyers over the past few years: You can’t take low mortgage rates for granted. After several years of rates below 5% (with periods even below 3%), current rates are a reminder that it’s not only home prices that matter in home affordability calculations. Borrowers can take some steps to ensure they qualify for the lowest rates available, but lenders will only go so low. Home down payments are another input that can have a considerable impact on how much buyers spend each month.

Increasing a down payment from 8% to 12%, for example, can shave several hundred dollars off of the monthly housing cost. But if possible, increasing your down payment to 20% can eliminate the PMI requirement on a conventional loan.

First-time home buyer tip: To be sure, putting 20% down on a high-priced home won’t be possible for all first-time buyers. It’s an especially tall order when homes are priced as high as they are now. But the larger your down payment, the less you have to finance, and every bit helps. So, for instance, if you’re waiting for mortgage rates to come down a bit, using that time to intentionally squirrel away more in savings means you can also take out a smaller loan when you’re ready to start shopping. If you hope to buy in the coming months, keeping your down payment fund in a high-yield savings account ensures it’s readily available. But if you plan on waiting a year or two and can stand putting the money out of reach, a certificate of deposit may offer higher rates.

Inventory deficit remains the driver of high prices

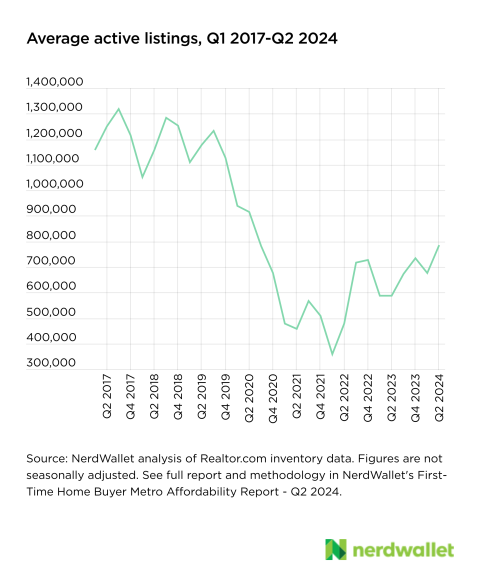

The high home prices we currently see are a direct result of too few homes. This low supply in the face of high demand drives prices up. And currently, the supply is so low that even seasonal quarterly gains in inventory aren’t enough to provide relief.

The second quarter of the year generally brings more listings to the market, and Q2 of 2024 was no different. Across the country, the number of homes on the market rose by 17% compared with the previous quarter, and a generous 34% compared to last year’s second quarter. Despite these gains, list prices rose 4% in the second quarter.

While inventory continues to climb, the current number of homes on the market at any given time is still at a significant deficit from where it was before the pandemic.

First-time home buyer tip: In the past, first-time buyers began their homeownership journey with a “starter” home — something smaller or a home that needed some work — to help keep the price point reasonable. But in this market where homes are few and far between, starter homes are difficult to find. One way to increase the number of homes available to you is to expand your search. Whether geographically — looking at homes in different neighborhoods or even towns — or by considering home types or features that aren’t on your long-term wishlist, the more flexible you are in your homebuying journey, the more likely you are to find something that fits the bill.

The analysis methodology is available in the original article, published at NerdWallet.

More From NerdWallet

Elizabeth Renter writes for NerdWallet. Email: elizabeth@nerdwallet.com. Twitter: @elizabethrenter.

The article Q2 Affordability Obstacles Hinder Would-Be First-Time Home Buyers originally appeared on NerdWallet.